What is the Gender Pension Gap?

What is the gender pension gap? On the surface, it’s exactly what you’re reading: a gap in pension funds between men and women, with men having more pension funds to retire with than women. Beneath the surface, though, the gender pension gap is what happens when lack of pay equity during a woman’s career catches up with her in old age. It’s the final insult to injury…systemic patriarchy hurts us until the very end.

Personally, retirement doesn’t scare me because it’s not something I’ll be able to financially achieve. Life handed me lemons, and as much as I try to make lemonade, it can’t possibly turn the tide of being left financially decimated at 50. What really scares me though is old age and the loss of the ability to work to support myself. I often find myself wide awake, worried about sleeping on the streets someday. This is not hyperbole, and I am not alone.

According to a study from HSBC, “One out of every two (50%) working-age Canadian women is worried that they will not have enough money to cover their medical or care expenses in retirement. In addition, the survey results show that more than two-fifths (44%) of Canadian women fear that they will struggle to pay for basic necessities during retirement compared to 37% of men.”

And as if that weren’t enough, even women who have worked their whole lives and contributed to a pension get the short end of the stick. The gender pension gap is real, and the consequences are terrifying. It’s just one of many reasons that total pay equity needs to be reached. Lack of equity doesn’t just impact your hourly wage; it has a very real impact on your ability to retire and stay retired.

Insights from the Ontario Pay Equity Office Report

The Ontario Pay Equity Office recently published a comprehensive report examining the gender pension gap. As of 2021, the gender pension gap in Canada is approximately 17%, and despite women’s increased participation in the workforce, the gap has not significantly narrowed since it was first measured at 15% in 1976. The report identifies two primary obstacles to closing this gap: Canada’s increasing reliance on private pensions, which are the most gender-unequal component, and women’s unequal share of unpaid family care work, which limits their ability to increase paid work and pension contributions.

Global Context and Impact

According to the Mercer CFA Institute 2023 Global Pension Index, Canada ranks 12th out of 47 countries in pension system effectiveness. In 2021, the gender pension gap in Canada was reported as 17% by Statistics Canada and 21.8% by the OECD. Comparatively, the average gender pension gap across 34 OECD countries was 25.6%, with Estonia having the lowest gap at 3.3% and Japan the highest at 47.4%.

The gender pension gap has a disproportionate impact on women’s financial security. In 2020, there were 200,000 more women aged 65 and older living below Canada’s low-income cut-off than men. Additionally, 21% of women aged 75 and older had incomes below the low-income cut-off, which is 51% higher than men of the same age.

These statistics underscore the critical need for systemic changes to address the gender pension gap and ensure financial equity for all Canadians in their retirement years.

The 17% Gap: A Closer Look

The gender pension gap currently sits at 17%. This means for every dollar of retirement income that a man receives, a woman will receive only 83 cents. Now think about the current cost of living and then how a gap like this impacts shelter, food, and medical care decisions every day. This isn’t a minor difference.

And this disparity has remained stubbornly persistent, even as the gender wage gap has shown signs of narrowing over the years. Back in 1976, the gender pension gap was measured at 15%, showing that it has actually widened over time despite increased female participation in the workforce.

Contributing Factors to the Gender Pension Gap

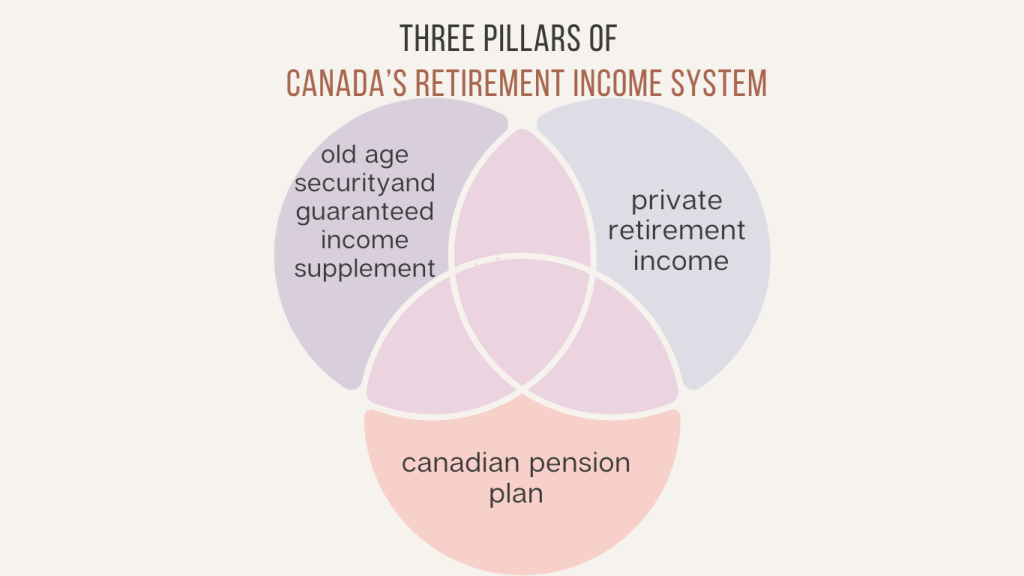

The gender pension gap arises from multiple factors. One major contributor is the design of the Canadian retirement system, which is heavily dependent on labour market earnings. Public pensions like the Canada Pension Plan (CPP) are tied to time worked and compensation level over a lifetime, which tends to favour men due to their longer, uninterrupted careers. Don’t even get me started on how women are financially punished for raising families in the short and long term. Is it any wonder women are opting out of marriage and kids, but I digress.

Women’s increased responsibilities in unpaid caregiving work also limit their ability to accumulate pension benefits. Moreover, private pensions, which form a large part of retirement income, disproportionately benefit those who have spent their entire careers with one employer, a situation more common among men.

The Need for Systemic Change

Addressing the gender pension gap requires systemic policy changes. It’s not just about what individual women can do; it’s about recognizing and correcting the gendered impacts of past policy decisions. Employers and financial institutions need to examine their retirement benefit structures for unintentional gender biases. Government bodies must revisit and revise policies from the 1960s that have contributed to this disparity. By doing so, we can create a more equitable system that supports all Canadians in their retirement years.

The Path Forward: How to Fix the Gender Pension Gap

How Women Can Protect Themselves

- Start Early and Save Consistently Begin saving for retirement as early as possible and contribute as much as you can afford. The power of compounding means your investments grow over time, and starting early gives your money more time to grow.

- Maintain Regular Pension Contributions Avoid gaps in your pension contributions, especially during your 20s and 30s. Plan for career breaks and ensure you continue contributing whenever possible, even during periods of reduced income or workforce absence.

- Maximize Employer Contributions Take advantage of any employer-matching contributions to your pension. This is essentially extra income that you would miss out on if you don’t contribute enough to trigger the employer match.

- Increase Contributions with Pay Raises Consider increasing your pension contributions whenever you receive a pay raise. For example, if you get a 3% raise, try to allocate at least 1% of it towards your pension. This small adjustment can significantly boost your retirement savings over time.

- Track Down Lost Pensions Keep track of all your pension accounts, even those from previous employers. Finding and consolidating lost pensions can substantially increase your total retirement savings.

- Partner Discussions Discuss financial planning, including savings and pensions, with your partner to ensure both of you can contribute to your retirement funds.

- Awareness on Divorce Implications Greater awareness is needed on how divorce affects pensions. Both partners should be aware of how their retirement savings might be impacted.

Stay informed about your financial situation and take an active interest in managing your money to make it work harder for you.

How Government and Employers Can Step it Up

- Close the Gender Wage Gap. Simply put this is a no-brainer but here we are, still fighting to address the obvious.

- Flexible Work Models Introduce personalized models for employees that clearly show the impact of different working arrangements and career gaps on pay and pensions.

- Legislative Support Our government should enact laws to make all jobs flexible and improve pay rates for low-income roles, ensuring fairer pension accumulation for all.

- Revise Pension Policies Pension plan administrators should consider unisex rates for annuities, ensure survivor benefits, and index pensions to inflation.

Stay Informed and Spread the Word

To stay up to date and learn more about the efforts being made to address the gender pension gap, visit Ontario’s Pay Equity Office. By spreading the word and staying informed, we can work together to create a more equitable future for everyone.

DISCLOSURE: THIS ARTICLE IS THE THIRED IN A THOUGHT-PROVOKING 6-PART SERIES BROUGHT TO YOU IN PARTNERSHIP WITH THE PAY EQUITY OFFICE OF ONTARIO. AS PART OF THIS COLLABORATION, I AM BEING COMPENSATED FOR MY EFFORTS TO SHED LIGHT ON THE CRUCIAL ISSUES SURROUNDING PAY EQUITY AND TO CONTRIBUTE TO THE BROADER CONVERSATION ON ACHIEVING GENDER EQUALITY IN THE WORKPLACE.